- 연말 절세 계획(Year-End Tax Planning)15242017.12.01

- 2017 및 2018 중요 세법 & 노동법 변경 사항13752017.12.13

- 비트코인(Bitcoin)과 세금(Tax)20262017.12.14

- 비트코인(Bitcoin)과 트럼프 세법(Tax Cuts and Jobs Act)11652017.12.26

- 트럼프 세제 개혁안(Tax cuts and jobs act)13962017.12.21

비트코인(Bitcoin)과 세금(Tax)

2017.12.14비트코인(Bitcoin)과 세금(Tax)

전 세계가 가상통화인 비트코인 열풍에 휩싸여 있습니다. 최근 뉴스에서 비트코인의 투기적 현상과 문제점들에 대해서 다루고 있지만, 비트코인에 대한 관심과 열기는 쉽게 사라질 것 같지 않습니다. 그렇다면 비트코인 투자로 인해 발생하는 수익 또는 손실에 대해 미국 국세청은 어떤 입장을 취하고 있는지 알아보겠습니다.

2014년 미국 국세청(IRS)는 가상화폐에 관한 세금 가이드를 발표합니다. 이 가이드는 가상화폐에 대한 유일한 미 국세청의 공식입장으로 그 내용은 아래와 같습니다.

- 연방세금 목적상 가상화폐는 자산(property)로 간주하고, 가상화폐 거래에 일반적인 자산 거래와 같은 세법규정을 적용한다(세금목적상 가상화폐는 화폐(currency)로 인정하지 않지 않음)

- 가상화폐 거래에서 발생하는 수익과 손실의 성격은 납세자가 가상화폐를 투자자산(capital asset)으로 소유하고 있었는지 여부에 따라 결정된다.(즉, 가상화폐를 투자 목적으로 소유했는지 아니면 단지 화폐처럼 결제의 수단으로 소유하고 있었는지가 중요)

- 직원이 가상화폐로 월급을 받은 경우 과세하고 고용주는 W-2폼을 발행해야 한다. 비지니스 비용으로 서비스 공급업자에게 가상화폐로 비용을 지급한 경우, 비지니스 오너는 지불 금액이 $600이상인 경우에는 1099폼을 발급해야 한다.

- 세금보고 시 가상화폐의 가치는 월급 또는 비용을 받은 날짜의 공정시장가격(fair market value)로 보고한다.

- 가상화폐를 채굴(mining)하는 납세자의 경우 가상화폐를 채굴한 날짜의 공정시장가격에서 채굴에 필요한 경비를 제한 순수익에 대해 납세의 의무가 발생한다.

2015년 세금보고에서 802명의 미국 납세자만이 비트코인 거래에서 발생한 수익과 손실을 보고했다고 합니다. 그 후 미국 국세청은 Chainalysis와 계약을 맺고 비트코인 소유주들에 대한 정보를 받고 있다고 하니 2017년 세금보고 시에 주의하시기 바랍니다.

Peter Sohn, CPA

Tel:213-487-3690 E-mail:petersohncpa@gmail.com

IR-2014-36, March. 25, 2014

WASHINGTON — The Internal Revenue Service today issued a notice providing answers to frequently asked questions (FAQs) on virtual currency, such as bitcoin. These FAQs provide basic information on the U.S. federal tax implications of transactions in, or transactions that use, virtual currency.

In some environments, virtual currency operates like “real” currency -- i.e., the coin and paper money of the United States or of any other country that is designated as legal tender, circulates, and is customarily used and accepted as a medium of exchange in the country of issuance -- but it does not have legal tender status in any jurisdiction.

The notice provides that virtual currency is treated as property for U.S. federal tax purposes. General tax principles that apply to property transactions apply to transactions using virtual currency. Among other things, this means that:

- Wages paid to employees using virtual currency are taxable to the employee, must be reported by an employer on a Form W-2, and are subject to federal income tax withholding and payroll taxes.

- Payments using virtual currency made to independent contractors and other service providers are taxable and self-employment tax rules generally apply. Normally, payers must issue Form 1099.

- The character of gain or loss from the sale or exchange of virtual currency depends on whether the virtual currency is a capital asset in the hands of the taxpayer.

- A payment made using virtual currency is subject to information reporting to the same extent as any other payment made in property.

- 1예수님

- 22019 세금보고

- 3666짐스표

- 4여배우 아내 길들…

- 5대한항공 주가 및…

- 6가성비블라인드

- 7일상

- 8뉴저지

- 9故정재윤(방송인)…

- 10경제

-

[내 마음의 隨筆] <디지털 연료를 쓰는 시대 — 토큰과 프롬프트의 지혜> 1 of 2

[내 마음의 隨筆]디지털 연료를 쓰는 시대 — 토큰과 프롬프트의 지혜아침에 스마트폰을 켜고 ChatGPT와 같은 인공지능에게 질문을 던지는 순간, 우리는 이미 보이지 …

[내 마음의 隨筆] <디지털 연료를 쓰는 시대 — 토큰과 프롬프트의 지혜> 1 of 2

[내 마음의 隨筆]디지털 연료를 쓰는 시대 — 토큰과 프롬프트의 지혜아침에 스마트폰을 켜고 ChatGPT와 같은 인공지능에게 질문을 던지는 순간, 우리는 이미 보이지 …

-

어머니날

https://youtu.be/7PCi5Z4YvlY?si=1EC1pW15202uloAH

어머니날

https://youtu.be/7PCi5Z4YvlY?si=1EC1pW15202uloAH

-

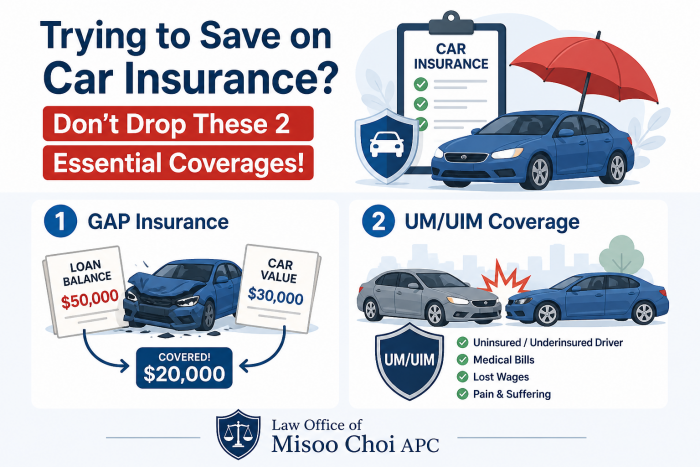

캘리포니아 차 보험료 인상... 이 두 가지 옵션만은 절대 빼지 마세요

최근 캘리포니아의 자동차 보험료 부담이 커지면서, 갱신 때마다 보험료를 낮추기 위해 가장 기본적인 최소 책임보험(Minimum Liability)만 남기고 주요 옵션들을 제외하는…

캘리포니아 차 보험료 인상... 이 두 가지 옵션만은 절대 빼지 마세요

최근 캘리포니아의 자동차 보험료 부담이 커지면서, 갱신 때마다 보험료를 낮추기 위해 가장 기본적인 최소 책임보험(Minimum Liability)만 남기고 주요 옵션들을 제외하는…

-

하와이좋은교회 이야기, HAWAII GOOD CHURCH

https://youtu.be/FJtamYt1SmE?si=VGsR_AUpoz-SBle9

하와이좋은교회 이야기, HAWAII GOOD CHURCH

https://youtu.be/FJtamYt1SmE?si=VGsR_AUpoz-SBle9

-

영주출장홈타이™20대™라인:LUP25™영주유흥업소™영주룸싸룽™영주여대생출장안마™영주출장만남후기™

영주출장홈타이™20대™라인:LUP25™영주유흥업소™영주룸싸룽™영주여대생출장안마™영주출장만남후기™영주출장…

영주출장홈타이™20대™라인:LUP25™영주유흥업소™영주룸싸룽™영주여대생출장안마™영주출장만남후기™

영주출장홈타이™20대™라인:LUP25™영주유흥업소™영주룸싸룽™영주여대생출장안마™영주출장만남후기™영주출장…

-

Threema ID: FA8K9CNT /依托咪酯 我有技术 | 我要技术 CAS:33125-97-2 ,英文名 , etomidate ,space oil ,CAS: 33125-97-2

Threema ID: FA8K9CNT Signal ID: Drmcdonald.52 Email ..Evgglobalchemist@proton.me Session ID:0…

Threema ID: FA8K9CNT /依托咪酯 我有技术 | 我要技术 CAS:33125-97-2 ,英文名 , etomidate ,space oil ,CAS: 33125-97-2

Threema ID: FA8K9CNT Signal ID: Drmcdonald.52 Email ..Evgglobalchemist@proton.me Session ID:0…

-

은퇴 자산 50만 달러 지키는 방법? 은퇴는 저축이 아니라 설계입니다

많은 사람들이 은퇴 준비를 이야기할 때 가장 먼저 수익률을 떠올립니다. 더 높은 수익을 얻고 더 많은 자산을 모아야 안정적인 노후를 보낼 수 있다고 생각하기 때문입니다.물론 자산…

은퇴 자산 50만 달러 지키는 방법? 은퇴는 저축이 아니라 설계입니다

많은 사람들이 은퇴 준비를 이야기할 때 가장 먼저 수익률을 떠올립니다. 더 높은 수익을 얻고 더 많은 자산을 모아야 안정적인 노후를 보낼 수 있다고 생각하기 때문입니다.물론 자산…

-

2026년▶⑤◀Memorial Day추모

너무 많아서 헤아릴 수 없는 추모자들~그래도 할 수 있을 지점까지 찾아 본추모자들을 차근히 기술해 보기로!故Richard G. Cushman (SFC) 1932년2월29일~195…

2026년▶⑤◀Memorial Day추모

너무 많아서 헤아릴 수 없는 추모자들~그래도 할 수 있을 지점까지 찾아 본추모자들을 차근히 기술해 보기로!故Richard G. Cushman (SFC) 1932년2월29일~195…

-

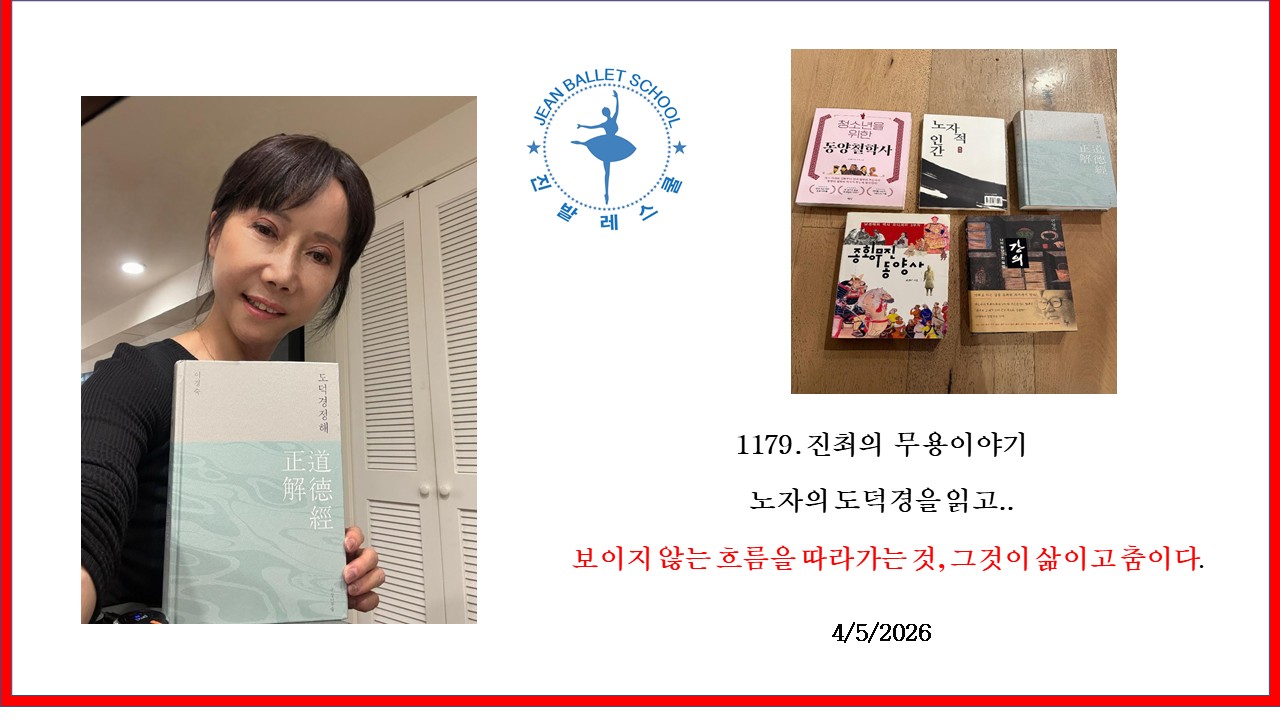

1179.노자의 도덕경을 읽고.. 보이지 않는 흐름을 따라가는 것, 그것이 삶이고 춤이다.

보이지 않는 흐름을 따라가는 것, 그것이 삶이고 춤이다. 노자의 도덕경을 읽고..독서 모임 덕분에 지난해 장자를 읽었고, 이번에는 노자의 도덕경을 읽기 시작했다. 그렇게 나는 다…

1179.노자의 도덕경을 읽고.. 보이지 않는 흐름을 따라가는 것, 그것이 삶이고 춤이다.

보이지 않는 흐름을 따라가는 것, 그것이 삶이고 춤이다. 노자의 도덕경을 읽고..독서 모임 덕분에 지난해 장자를 읽었고, 이번에는 노자의 도덕경을 읽기 시작했다. 그렇게 나는 다…

-

선우 권 목사 초청 기도 집회

할렐루야!선우권 목사 초청제2차 돌파 기도 영성집회성령님의 인도하심 가운데 하나님께 간절히 기도하며,삶의 회복과 돌파를 경험하는 은혜의 자리로 여러분을 초청합니다.기도 응답을 사…

선우 권 목사 초청 기도 집회

할렐루야!선우권 목사 초청제2차 돌파 기도 영성집회성령님의 인도하심 가운데 하나님께 간절히 기도하며,삶의 회복과 돌파를 경험하는 은혜의 자리로 여러분을 초청합니다.기도 응답을 사…

Ktown1번가 대표이메일 webinfo@koreatimes.com | 업소록 문의 yp@koreatimes.com

Powered by The Korea Times. Copyright ©The Korea Times All rights reserved.